The mining sector in South America, particularly in countries like Peru and Chile, faces a complex landscape in 2025. On one hand, there is notable growth and strong investment projections, but on the other, there are serious internal challenges and external pressures that could jeopardize this progress. While the sector is key to the region’s economies, this commercial crisis and the fluctuation of commodity prices are limiting growth opportunities and demanding a rethinking of the mining model.

Growth and Opportunities: The Optimistic Side of the Mining Sector

Despite the headwinds, the South American mining sector, especially in Peru and Chile, shows strong vitality. In Peru, mining employment reached a record high of over 242,000 people in early 2025, and each mining job is estimated to generate about eight more in related sectors. The investment pipeline is also impressive, with 14 new mining projects set to begin between 2026 and 2029, representing more than $14.6 billion in investment. With the inclusion of all planned developments through 2029, the figure climbs to nearly $20 billion. Major projects like Tía María, Corani, and Ampliación Ilo are either already underway or nearing final approvals. Furthermore, copper exploration is booming, with 84 initiatives in development and a combined investment of over $600 million concentrated in regions like Ica, Arequipa, Apurímac, and Áncash.

Inherent Challenges and the Influence of the Crisis

Mining growth is intertwined with a number of unresolved issues that become more critical in an economic crisis environment.

Illegal Mining and Formalization

Illegal mining and informality are among the biggest challenges in Peru. It has become a major threat to the discovery of new mineral resources, as the presence of informal operations in some areas makes it nearly impossible for formal companies to operate. The REINFO system (Registro Integral de Formalización Minera), which sought to bring small-scale and artisanal miners into the formal economy, has largely failed to meet its objectives. As of early 2025, over 61,000 miners were suspended from REINFO, and many may still be operating without oversight. The program has been criticized for becoming a “shield of impunity”, allowing miners to operate without meeting environmental or safety standards, as long as they maintain their status in the registry. The Peruvian government has announced that REINFO will be definitively terminated on December 31, 2025, marking a turning point for the sector. The new approach will seek greater oversight and the integration of data from multiple state entities to improve the traceability of mining activity and the gold extracted.

Environmental Liabilities

Another urgent issue is the remediation of environmental liabilities. The government has officially logged more than 6,000 environmental liabilities from past mining, and estimates suggest over 87,000 more could be linked to informal mining under REINFO. The total cleanup bill could exceed $43 billion, which is nearly half of Peru’s net international reserves. Progress has been painfully slow. The state-run remediation agency, Activos Mineros, has spent over S/ 800 million without securing a single closure certificate, and private companies have only closed three liability sites.

Industry Response and the Role of Sustainability

In an attempt to mitigate these risks and respond to pressures, mining companies are investing in environmental management, innovation, and community partnerships. Companies like Anglo American have invested more than S/ 2.5 billion in local purchases and over S/ 249 million in social programs in Moquegua since 2018. They have supported the development of an AI-powered water management system to detect leaks and predict pipe failures. Cerro Verde has earned 17 patents for technologies that improve safety and reduce environmental risks, while Gold Fields spent over S/ 100 million in 2024 on local goods and services.

The circular economy is also gaining ground, with Peru’s Ministry of Environment launching a national roadmap for a transition to circular production models by 2030. Mining companies are responding with initiatives focused on waste reduction, digital traceability, and local supply chains.

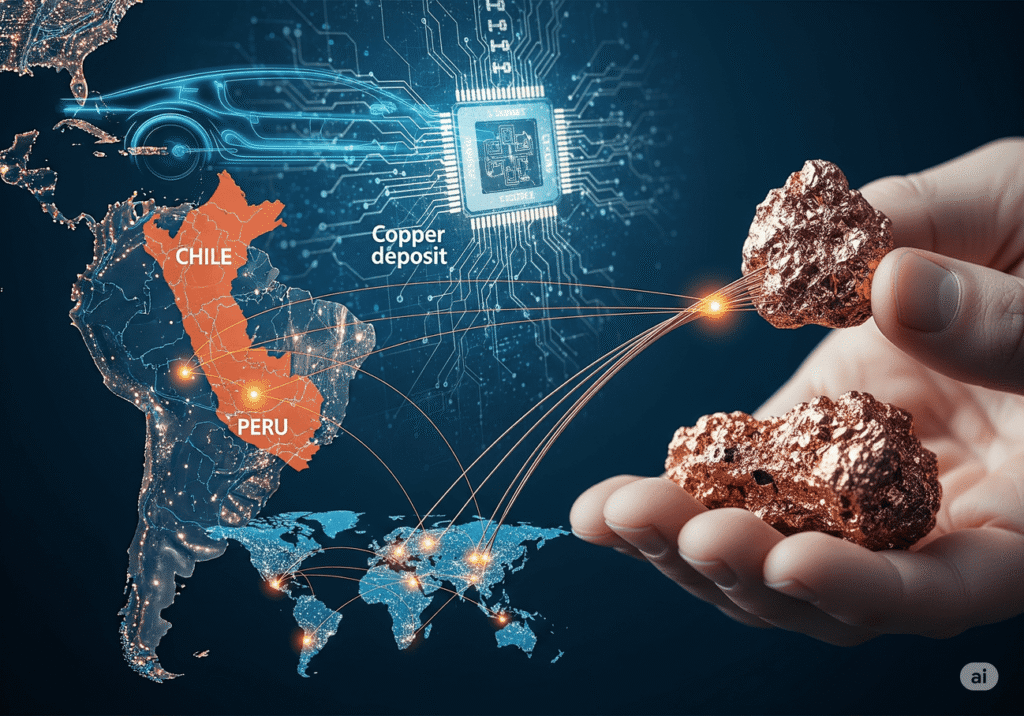

The Copper Outlook and Regional Competition

The global economic crisis and growing copper demand for the energy transition place Chile and Peru in a key position, as together they produce nearly 40% of the world’s copper. However, both countries face challenges. Chile, although the world’s leading producer, is grappling with aging mines, lower ore grades, and a lack of major new discoveries. Political uncertainty around tax regimes and environmental regulations also affects investment. Peru, for its part, has vast untapped copper reserves and projects that could double its output by 2037. However, progress is slow due to social unrest, bureaucratic bottlenecks, and delays in environmental permitting.

Competition for high-quality copper concentrates has intensified. The shortage of concentrate has led Chinese smelters to negotiate processing fees nearing zero with Chilean producers, a sign of how tight the market has become. This presents a paradox for miners: prices are rising, but so are costs, and the competition for quality concentrate is fierce. Companies capable of producing clean, high-grade concentrates, such as Element 29 Resources, are well-positioned to thrive.

In addition, junior mining companies are playing an important role in exploration, using advanced technologies to find new deposits. Firms like Chakana Copper and Hannan Metals are exploring porphyry and breccia systems that could become key assets and attract major miners.

The Future: ESG Leadership and Collaboration

The economic crisis underscores the need for South American mining to be not only productive but also responsible and sustainable. Investors are now paying close attention to ESG (environmental, social, and governance) performance. Companies with strong ESG practices are accessing “green capital” and building reputational advantages. In this regard, Peru is making progress with initiatives such as redefining the role of mining in regional development, shifting from “mining corridors” to “development corridors” that prioritize health, infrastructure, and governance.

Despite the challenges, both countries have strategic assets. Chile benefits from mature mining infrastructure and the development of renewable energy sources like solar and wind to power its mines. Peru, for its part, has strategic assets like the new Chancay Mega Port, which will enhance export routes to Asia.

The future of the sector in South America will depend on the ability of governments and companies to address illegal mining, environmental remediation, regulatory reform, and the fostering of collaboration with communities. Success will not only require finding new copper deposits but also bringing them to market efficiently, responsibly, and with community support.